How I Built My First Product Without Betting the Farm

You’ve got a great product idea, but the fear of losing everything holds you back. I’ve been there—pouring savings into a dream with no safety net. That’s when I learned a game-changing lesson: you don’t have to risk it all to start. Through simple asset diversification, I funded my launch without sinking my finances. This is how I balanced risk, protected my income, and still made it happen—no magic, just smart moves. It wasn’t about chasing overnight success or betting the house on a single idea. It was about making thoughtful, measured decisions that allowed growth without collapse. And if you’re someone who values stability as much as ambition, this approach isn’t just safer—it’s smarter, more sustainable, and ultimately more rewarding.

The Rookie Mistake: Putting All Eggs in One Product Basket

Every great product begins with a spark—an idea so compelling it feels like destiny. But too often, that excitement becomes a trap. The most common misstep among first-time creators is treating their idea like an all-or-nothing proposition. They believe that to prove commitment, they must go all-in: cash out retirement accounts, max out credit cards, borrow from relatives, or quit their jobs before the first prototype exists. This mindset, while passionate, is dangerously flawed. History shows us that even brilliant ideas can fail—not because they lack potential, but because the financial foundation beneath them crumbles too soon.

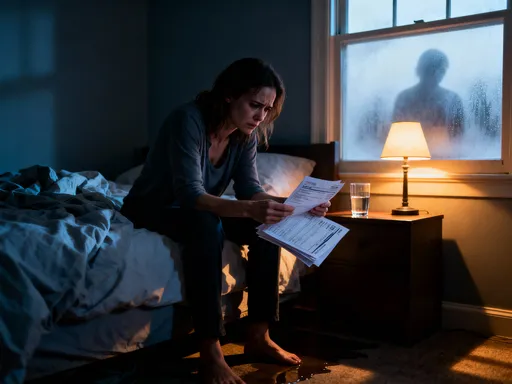

Consider a real-life scenario: a woman in her early 40s with years of experience in home organization develops a smart storage system she’s convinced will revolutionize small-space living. Excited and driven, she invests $35,000 of her savings into tooling, manufacturing, and initial inventory. She skips paying herself, cuts back on family expenses, and takes on extra debt to cover marketing. Months pass with slow sales. A competitor launches a similar product at a lower price. Her distribution partner pulls out. Without a backup plan or alternative income, she’s forced to shut down, leaving her financially strained and emotionally drained. This isn’t an outlier—it’s a pattern repeated across industries and experience levels.

Why is this approach so risky? Because it ignores two fundamental truths: markets are unpredictable, and product development is iterative. Unexpected delays, shifting consumer preferences, supply chain issues, or regulatory hurdles can derail even the best-laid plans. When all your resources are tied to one outcome, any setback becomes catastrophic. There’s no room for adaptation, no buffer for learning, and no margin for error. The emotional toll is just as damaging. Financial pressure breeds desperation, which leads to rushed decisions—like lowering prices too soon, skipping quality checks, or launching before the product is truly ready. Instead of building something strong, you’re trying to outrun collapse.

Moreover, this all-in strategy often stems from a cultural myth: that real entrepreneurs always bet big. We’re fed stories of founders who mortgaged homes and lived on ramen to build empires. While those tales inspire, they rarely reflect the full picture. For every high-profile success, there are countless others who took the same leap and disappeared without a trace. The truth is, long-term success rarely comes from a single, massive gamble. It comes from resilience, consistency, and the ability to endure setbacks without falling apart. And that kind of endurance requires financial stability, not recklessness.

Asset Diversification Isn’t Just for Wall Street

When most people hear “asset diversification,” they think of stock portfolios—spreading investments across different industries or asset classes to reduce risk. But this principle applies far beyond Wall Street. For entrepreneurs, diversification is a practical survival strategy, not just an abstract financial concept. It means consciously distributing your resources—time, money, skills, and income streams—so that no single failure can knock you off course. It’s the difference between building on bedrock versus building on ice.

In the context of product development, asset diversification means avoiding total dependence on one funding source, one income stream, or one idea. Instead, it involves creating layers of support. For example, using a portion of side-income profits to fund development, keeping a part-time job to maintain health benefits and steady cash flow, or maintaining a mix of liquid and fixed assets to ensure flexibility. This approach doesn’t dilute your commitment—it strengthens it by giving you the breathing room to make thoughtful decisions.

Contrast this with the “bet-it-all” model. In that scenario, every dollar, every hour, and every ounce of emotional energy is poured into a single venture. If it succeeds, the payoff may be large. But if it stalls or fails, the consequences are severe—not just financially, but personally. You lose savings, confidence, and sometimes relationships. With diversification, failure of one component doesn’t mean total collapse. You might lose a small investment in a prototype, but your core stability remains intact. You can learn, adjust, and try again.

Real-life examples show how small shifts in resource allocation make a big difference. One mother in Ohio developed a line of natural cleaning wipes after noticing gaps in eco-friendly home products. Instead of quitting her remote administrative job, she used her overtime pay to fund small-batch production. She tested the product at local markets, reinvested early profits, and gradually scaled. Because she wasn’t dependent on the product’s immediate success, she could afford to refine the formula, gather feedback, and build a customer base slowly. Two years later, her brand is available in regional stores—and she still has her job, her health insurance, and her peace of mind.

Another example: a teacher in Colorado wanted to launch a curriculum-based board game for elementary classrooms. Rather than taking out a loan, he used income from weekend tutoring and summer workshops to cover design and patent costs. He launched a modest pre-sale campaign, which validated demand without requiring mass production. By spreading costs over time and using existing income streams, he minimized risk and maintained control. Today, his game is used in over 200 schools, and he’s exploring licensing opportunities—all without ever feeling financially cornered.

These stories aren’t about playing it safe. They’re about playing it smart. Diversification doesn’t eliminate risk—it manages it. It replaces panic with patience, desperation with discipline. And for many aspiring creators, especially those with family responsibilities or limited financial cushions, that balance is not just wise—it’s essential.

Mapping Your Financial Ecosystem Before Building

Before sketching a product design or writing a business plan, the most important step is often overlooked: auditing your financial ecosystem. This means taking a clear, honest look at your current financial position—what you earn, what you own, what you owe, and what you can afford to lose. Too many people jump into entrepreneurship without this foundation, assuming that passion will cover the gaps. But passion doesn’t pay bills. A solid financial map does.

Start by listing all sources of stable income. This includes salaries, freelance gigs, rental income, or any consistent cash flow. Next, assess your assets: savings accounts, retirement funds, home equity, vehicles, or other valuable possessions. Then, review your liabilities—credit card debt, loans, mortgages, or other obligations. The goal isn’t to judge yourself but to understand your starting point. How much monthly income is truly discretionary? How much savings can you access without penalty? What would happen if your main income source disappeared tomorrow?

One crucial metric is your emergency fund. Financial advisors often recommend three to six months’ worth of living expenses set aside for unexpected events. If you don’t have that, building a product should not be your next financial move. Instead, focus on strengthening that base first. A product can wait. Financial security cannot.

Once you know your baseline, identify which assets can support your project without endangering your stability. For example, if you have $10,000 in savings and $3,000 is your emergency cushion, then $7,000 might be available for investment—but only if you’re prepared to lose it. A smarter approach might be to allocate just 10%—$700—to initial research and prototyping, keeping the rest protected. This creates a psychological and financial boundary that prevents overreach.

Also consider time as an asset. How many hours per week can you realistically dedicate to your product without burning out or neglecting family responsibilities? If you have 10 hours, treat them like a limited resource. Prioritize tasks that deliver the highest return—like customer interviews, market testing, or low-cost prototypes—over expensive or speculative steps.

Mapping your financial ecosystem isn’t about limiting dreams. It’s about aligning them with reality. It transforms vague aspirations into actionable plans grounded in what’s possible. When you know your limits, you can innovate within them—finding creative, low-risk ways to move forward. And that clarity reduces anxiety, boosts confidence, and increases your chances of long-term success.

Funding Your Idea Without Draining Your Life Savings

Many people assume that launching a product requires a large upfront investment. But in reality, most successful ventures start small and grow gradually. The key is to match your funding method to your risk tolerance, project scale, and financial reality. You don’t need a six-figure budget to begin—you need a smart, sustainable approach to financing.

One of the most effective strategies is reinvesting profits from side-income activities. If you already have a freelance gig, a part-time job, or a small online store, set aside a fixed percentage of earnings—say, 15%—for your product development. This turns steady income into slow but reliable capital. Because the money comes from surplus, not savings, you’re not putting your foundation at risk. Over time, even modest contributions add up. $200 per month becomes $2,400 in a year—enough to cover design, initial materials, or a small marketing test.

Another powerful method is pre-sales. Instead of spending thousands to produce inventory, offer your product as a pre-order. This does three things: validates demand, generates cash flow, and funds production. Platforms like Kickstarter or Etsy allow creators to test interest with minimal investment. A woman in Georgia used this model to launch a line of reusable baking mats. She created a simple video, set a $5,000 funding goal, and offered early-bird pricing. Within 30 days, she raised $12,000—enough to cover manufacturing and shipping without touching her savings. More importantly, she entered the market with confirmed buyers, not guesses.

Microloans are another low-risk option, especially for women-owned or small businesses. Organizations like Kiva or local credit unions offer small loans—often under $10,000—with favorable terms. Unlike credit cards, which can spiral with high interest, these loans are structured, predictable, and manageable. The key is to borrow only what you need and have a clear repayment plan. A $3,000 loan to fund mold creation for a kitchen gadget is reasonable if you expect sales to cover it within six months. A $15,000 loan with no revenue stream is dangerous.

Early supporters—friends, family, or loyal customers—can also provide funding through small investments or advance purchases. The difference here is relationship-based trust. Instead of asking for donations, offer value: exclusive access, personalized versions, or future discounts. This builds community while funding growth. One designer in Michigan raised $8,000 from 40 customers who pre-ordered her handmade pet collars. She delivered on time, maintained quality, and turned those early backers into long-term advocates.

The lesson is clear: slow and steady funding beats reckless spending. When you avoid draining your life savings, you maintain control. You can pause, adjust, or pivot without fear of ruin. And because you’re not desperate for immediate returns, you can focus on building something people truly want—not just something that sells fast.

Balancing Risk: When to Invest and When to Hold Back

Not every stage of product development requires the same level of investment. In fact, one of the biggest financial mistakes is spending heavily too early—on professional packaging, mass production, or paid ads—before validating the core idea. This is where the concept of phased investment becomes critical. It means releasing funds in stages, tied to real progress and customer feedback, not assumptions or enthusiasm.

Start small. Use minimal funds to create a prototype—whether it’s a 3D-printed model, a hand-sewn sample, or a digital mockup. Then, test it with real people. Get honest reactions. Ask: Would you buy this? At what price? What would make it better? This feedback is more valuable than any market report. If people aren’t excited, you’ve saved yourself from a much larger investment. If they are, you’ve gained confidence and direction.

Next, move to a pilot launch. Produce a small batch—50 or 100 units—and sell them directly through local markets, online platforms, or word of mouth. Track sales, gather reviews, and monitor repeat purchases. This phase tells you whether there’s real demand. If sales are strong, you can justify investing in better materials, larger production, or branding. If not, you can refine the product or reconsider the market fit—without major losses.

Only after validation should you scale. This could mean expanding distribution, hiring help, or launching a full marketing campaign. But even then, do it incrementally. Allocate budgets in phases: first $1,000 for photography and website updates, then $2,000 for targeted ads once traffic improves. This staged approach prevents overspending on unproven features and keeps your finances aligned with actual performance.

Phased investment also protects your decision-making. When you’re not under pressure to “make back” a huge upfront cost, you can stay objective. You’re not forcing a product on the market just to recoup expenses. You’re responding to data, not desperation. This leads to better quality, smarter pricing, and more sustainable growth.

Protecting Income While Growing Something New

Entrepreneurship doesn’t require sacrificing financial security. In fact, maintaining a stable income is one of the smartest things you can do while building a product. It reduces pressure, prevents emotional decision-making, and gives you the time to get things right. Whether through full-time employment, part-time work, or scalable side gigs, steady income is your safety net.

Many successful founders kept their jobs during the early stages of their ventures. They used their salary to cover living expenses, while channeling extra income or savings into their product. This allowed them to move at a sustainable pace, without the stress of needing immediate returns. One woman in Texas worked as a school counselor while developing a line of mindfulness journals for teens. She spent evenings and weekends on design and testing, used summer breaks for market research, and launched quietly through local schools. Three years later, her product is in bookstores nationwide—and she only left her job when revenue consistently exceeded her salary.

Freelancing is another flexible option. If you have skills in writing, design, consulting, or teaching, you can earn extra income on your own schedule. That income becomes fuel for your product—without the risk of total financial dependence. A man in Minnesota supported his outdoor gear startup by doing seasonal landscaping work. The physical labor gave him time to think, and the income funded small production runs. He never rushed to sell. He let demand grow naturally, and within four years, his brand gained a loyal following.

The key is balance. Allocate time wisely—protect your energy, set boundaries, and avoid burnout. Don’t try to do everything at once. Focus on progress, not perfection. And remember: a stable income doesn’t mean you’re not committed. It means you’re committed to doing it right.

Building Wealth Through Smart Choices, Not Big Risks

True wealth isn’t built in a single moment. It’s built through consistent, thoughtful decisions over time. The same is true for successful product ventures. The goal isn’t to win a high-stakes gamble—it’s to create something lasting, valuable, and resilient. And that kind of success comes not from how much you risk, but from how wisely you manage what you have.

Asset diversification isn’t just a risk management tool—it’s a long-term wealth-building strategy. By protecting your income, spreading your investments, and funding growth gradually, you create a foundation that supports innovation without sacrifice. You learn from failures without being destroyed by them. You adapt to change without losing your footing.

For many women, especially those balancing family, work, and personal goals, this approach is not just practical—it’s empowering. It proves that you don’t have to choose between stability and ambition. You can have both. You can build something meaningful without risking everything. You can grow wealth not through luck, but through discipline, patience, and smart allocation.

So if you have an idea, don’t wait for a windfall or a miracle. Start where you are. Use what you have. Protect your foundation. Invest wisely. And remember: the most enduring successes aren’t built on cliffs. They’re built on solid ground.