How I Regained Control After a Medical Emergency—My Real Financial Comeback

A sudden illness hit me hard—literally and financially. In days, my savings drained, bills piled up, and stress took over. I felt helpless, but I knew I had to act fast. What I learned wasn’t just about cutting costs or filing insurance claims—it was about rebuilding stability from the ground up. This is how I navigated the chaos, protected what mattered, and slowly restored my financial peace—without shortcuts or magic fixes. The journey wasn’t easy, but it was possible because I made deliberate, informed choices. This is not a story of overnight success, but of resilience, clarity, and practical steps that any family woman managing a household can apply when life throws a curveball.

The Shock of Sudden Illness: When Health Crumbles and Finances Follow

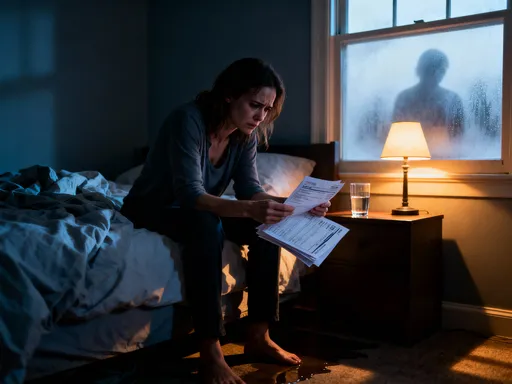

It started with what I thought was a bad flu. Fatigue, dizziness, a persistent fever—nothing I hadn’t experienced before. But within 48 hours, I was in the emergency room, diagnosed with a serious infection requiring immediate treatment and a two-week hospital stay. The physical toll was immense, but the financial shock that followed was just as debilitating. Before I could process my diagnosis, my bank account was being drained by hospital fees, specialist consultations, and unexpected medications not fully covered by insurance. My income stopped the moment I was admitted. I was self-employed, and without a formal sick leave policy, my earnings vanished overnight. The bills, however, did not.

What I didn’t realize at the time was how common this experience is. According to research from the Kaiser Family Foundation, nearly one in four Americans has struggled to pay medical bills, even those with health insurance. Insurance rarely covers everything—co-pays, deductibles, out-of-network charges, and non-covered treatments quickly add up. For someone already managing a household budget, a single medical crisis can unravel months or even years of careful financial planning. I had an emergency fund, but it was meant for car repairs or a broken appliance, not a prolonged illness. Within three weeks, it was gone. The emotional weight of this reality was crushing. I wasn’t just fighting to get well—I was fighting to keep my home, my credit, and my sense of control.

Many people believe that having insurance means they’re protected. But protection isn’t automatic—it’s earned through understanding, vigilance, and action. My crisis exposed a gap between having coverage and truly being covered. I had never read the fine print of my policy, never asked about pre-authorization requirements, and never considered the cost of follow-up care. When the bills arrived, I was blindsided. This is why financial vulnerability after a medical event is so widespread. It’s not just about income level; it’s about preparedness. The good news is that while the shock is real, the aftermath doesn’t have to be catastrophic. With the right steps, even in the middle of a crisis, it’s possible to stabilize and begin recovery.

First Moves: Stabilizing the Immediate Financial Bleeding

When a medical emergency strikes, the first 72 hours are critical—not just medically, but financially. This is when decisions can either contain the damage or allow it to spiral. My first instinct was to shut down, to focus only on healing. But I quickly realized that ignoring the financial side would only make recovery harder. I needed to act, even from my hospital bed. The first step was to stop the financial bleeding. That meant identifying which payments could be paused or delayed without triggering penalties or long-term consequences.

I began by calling my utility providers, my internet service, and my car insurance company. I explained my situation honestly and asked about hardship programs or temporary payment arrangements. To my surprise, most were willing to work with me. My electricity provider offered a deferred payment plan. My internet company reduced my bill for three months. My car insurance allowed me to suspend coverage temporarily because the vehicle wasn’t being driven. These weren’t permanent solutions, but they bought me breathing room. I also contacted my credit card issuers and mortgage servicer. I didn’t ask to cancel debts—I asked for forbearance. Most lenders have medical hardship policies, but you have to ask. Silence only leads to late fees and credit damage.

At the same time, I reached out to my doctor’s office and hospital billing department. I requested an itemized bill and asked about financial assistance programs. Many hospitals offer charity care or sliding-scale payments based on income. I also inquired about setting up a payment plan with zero interest. These conversations weren’t easy, especially while recovering, but they were necessary. Avoiding calls only leads to collection notices and stress. By taking control early, I prevented small balances from becoming unmanageable debt. The key lesson? Proactivity beats panic. You don’t need to solve everything at once—just take one step, then another. Each call, each email, was a small victory that restored a bit of control.

Insurance Reality Check: Getting the Most Without the Headache

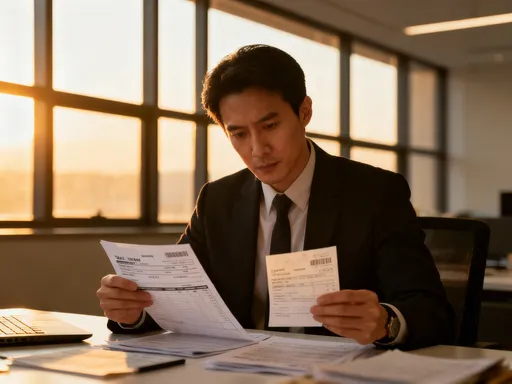

Health insurance is supposed to protect you, but only if you know how to use it. I learned this the hard way. After my hospital stay, I received a bill for over $12,000—my insurance had covered part, but I was responsible for the rest. I assumed it was correct. Then I reviewed the explanation of benefits and noticed something strange: a charge for a specialist consultation I never had. Another line item listed a procedure that was supposed to be fully covered under my plan’s preventive care clause. I dug deeper and found multiple errors. That’s when I realized: insurance companies make mistakes, and it’s your responsibility to catch them.

I requested an itemized bill from the hospital and cross-referenced every charge with my insurance policy. I called customer service and asked for a detailed breakdown of what was covered and why. I learned that some services were out-of-network because the hospital had used a contracted provider I didn’t authorize. I filed an appeal, submitting documentation that the treatment was medically necessary and should have been covered. It took six weeks, but I won. My out-of-pocket cost dropped by nearly $4,000. That wasn’t just money saved—it was a lesson in empowerment. Insurance isn’t a black box. You have the right to question, appeal, and negotiate.

I also discovered that many services could have been cheaper if done at an outpatient clinic instead of a hospital setting. For example, a blood panel billed at $800 in the hospital could have been done for $120 at a local lab. Going forward, I made it a rule to ask about alternative options and cost differences before any procedure. I also started keeping a file of all medical records, bills, and insurance correspondence. This made it easier to track claims and spot discrepancies early. The takeaway? Being an informed patient means being an informed consumer. You don’t need to be a lawyer or an accountant—just persistent and organized. A few hours of review can save thousands of dollars and reduce stress in the long run.

Income Interruption: Bridging the Gap When Paychecks Stop

When I stopped working, my income stopped too. That was the harsh reality. As a freelance writer, I didn’t have paid sick leave. My clients paused projects, and new ones dried up. I had no safety net from an employer, no automatic disability payments. The silence from my inbox was louder than any alarm. But I couldn’t afford to wait. I needed a way to bring in some income, even if it was small, without compromising my recovery.

First, I looked at what I already had. I had accrued vacation and personal days from previous years—about three weeks’ worth. I used those to apply for short-term disability through my professional association. It wasn’t much—around 60% of my average monthly income—but it was something. I also checked whether I qualified for state disability insurance. Some states offer partial wage replacement for non-work-related illnesses. The application was tedious, but once approved, it provided a modest but reliable monthly check. These formal benefits didn’t replace my full income, but they covered essentials like rent and groceries.

At the same time, I explored low-effort ways to earn extra. I didn’t have the energy for full projects, but I could handle small tasks. I offered editing services for short documents, created templates for other freelancers, and even sold digital planners online—work I could do in 30-minute bursts between rest periods. I also reached out to past clients and explained my situation. A few offered small retainer agreements, knowing I’d return to full capacity later. These weren’t high-paying gigs, but they kept me connected and brought in a few hundred dollars a month. The key was to focus on sustainability, not speed. I protected my health first, but I also refused to be passive. Income doesn’t have to be all or nothing. Even a trickle helps maintain dignity and reduces financial pressure.

Smart Spending Cuts: What to Trim Without Sacrificing Dignity

When income shrinks, spending must adjust—but not all cuts are wise. I learned that cutting too deeply, especially in areas that affect health and well-being, can backfire. For example, switching to a cheaper grocery store that lacks fresh produce might save money but harm recovery. The goal isn’t austerity; it’s strategic frugality. I needed to reduce expenses without sacrificing nutrition, mental health, or family stability.

I started by auditing my subscriptions. I had six streaming services, a meal kit delivery, a fitness app, and a magazine bundle. I canceled everything except one streaming platform and paused the rest. That saved over $100 a month with no real loss in quality of life. I also renegotiated my cell phone plan, switching to a lower-tier family plan through a relative. I called my cable provider and asked for a retention discount—something they offer to keep customers from leaving. These were painless changes that added up.

Groceries were a bigger challenge. I couldn’t eliminate food costs, but I could optimize them. I switched to a store with lower prices but good quality, used digital coupons, and planned meals around sales. I bought generic brands for non-sensitive items and focused on nutrient-dense, affordable foods like beans, eggs, frozen vegetables, and oats. I also reduced waste by repurposing leftovers and freezing portions. These changes saved about $200 a month. I also paused non-essential spending—no new clothes, no dining out, no home decor. But I didn’t cut everything. I kept a small budget for coffee, books, and family movie nights. Why? Because joy matters. Financial recovery isn’t just about numbers—it’s about morale. Deprivation leads to burnout. Discipline with compassion leads to sustainability.

Rebuilding the Safety Net: Starting Small, Staying Consistent

Once the immediate crisis passed, I faced a new challenge: rebuilding my emergency fund. The thought was overwhelming. How could I save when I was still catching up on bills? But I realized that waiting for “perfect” conditions meant never starting. So I began small—$10 a week, automatically transferred to a high-yield savings account. It felt symbolic, but it was powerful. That tiny amount represented a shift in mindset: from survival to forward motion.

I also used mental accounting to make saving easier. I labeled the account “Medical Buffer” instead of “Emergency Fund.” This made the purpose clear and urgent. I treated it like a non-negotiable bill, even if it was the last payment I made each month. Over time, I increased the amount as my income stabilized. I also set micro-goals—$100, then $500, then $1,000—celebrating each milestone. These wins built confidence and motivation.

Automation was key. I set up recurring transfers so I didn’t have to think about it. Even during months when money was tight, I kept the habit alive, even if the amount was reduced. Consistency mattered more than size. I also explored cash-back apps and small rewards programs, funneling those earnings into the fund. It wasn’t fast, but it was steady. Within 18 months, I had rebuilt a $5,000 buffer—enough to cover three months of essential expenses. More importantly, I had rebuilt my confidence. Saving wasn’t about perfection—it was about persistence. Every small deposit was a vote of trust in my future.

Long-Term Stability: Turning Crisis Into Financial Resilience

The medical emergency changed me—not just physically, but financially. It exposed weaknesses in my planning, but it also revealed strengths I didn’t know I had. Today, I’m not just recovered—I’m stronger. I have a clearer understanding of my insurance, a realistic emergency fund, and a more intentional approach to spending and saving. But the most important shift was in mindset. I no longer see financial stability as a destination. It’s a practice—a daily choice to be informed, proactive, and kind to myself.

I’ve taken preventive steps to reduce future risk. I upgraded my health insurance to include better coverage for specialist care and hospital stays. I added a critical illness rider, which provides a lump-sum payment if I’m diagnosed with certain conditions. I also created a financial binder for my family—listing accounts, policies, passwords, and emergency contacts—so they won’t be left in the dark if something happens again. These aren’t glamorous moves, but they’re protective. I also have regular check-ins with a financial counselor, not because I’m in crisis, but because maintenance matters.

This experience taught me that financial resilience isn’t about having the most money—it’s about having the right habits, the right knowledge, and the courage to act. A crisis doesn’t have to break you. It can clarify what matters, reset your priorities, and build a foundation that lasts. I wouldn’t wish what I went through on anyone. But if my story helps another woman facing a similar challenge feel less alone, less overwhelmed, and more in control—then the struggle had purpose. Stability isn’t magic. It’s made, one smart decision at a time.